Should You Avoid a Private Mortgage?

Private mortgages have seen a significant boom in recent years with 2018 being one of the largest spikes ever.

With the B20 stress test unveiled by the Office of the Superintendent of Financial Institutions at the end of December 2017, Canadians found themselves much more restricted on the amount they could borrow. In many cases buyers and borrowers were unable to access a mortgage at all from a traditional lender. The result for many was to turn to lenders who did not fall under the new stress test – credit unions and private lenders.

Credit unions, which are co-operatives owned by their members, saw a huge increase in new applications because they were able to qualify borrowers at the actual mortgage amount, rather than adding 2% to the rate for qualifying. As a result many credit unions took advantage by increasing their rates and began imposing their own restrictions and were able to pick from the best borrowers.

What is a Private Lender?

Those with challenging applications from weaker credit scores or income fluctuations were driven to the private lending sector. A private lender is essentially an individual or group who lends funds at their own discretion. They could be an individual lending out their own funds from a line of credit or even RRSP/RESP investments, or, more commonly they are institutional private lenders – corporations and investment pools.

We’ll discuss individual private lenders in another article. For the purposes here we’ll be referring to institutional lender; the most common type being Mortgage Investment Corporations (MICs). A MIC is a company that will borrow or manage funds in a pool and lend the funds out as mortgages. These companies manage the mortgage payments and take action when the borrower misses or is late with payments. The MIC will have underwriters who review mortgage and approve mortgage applications just as a traditional mortgage lender would and will receive a portion of the mortgage interest as compensation.

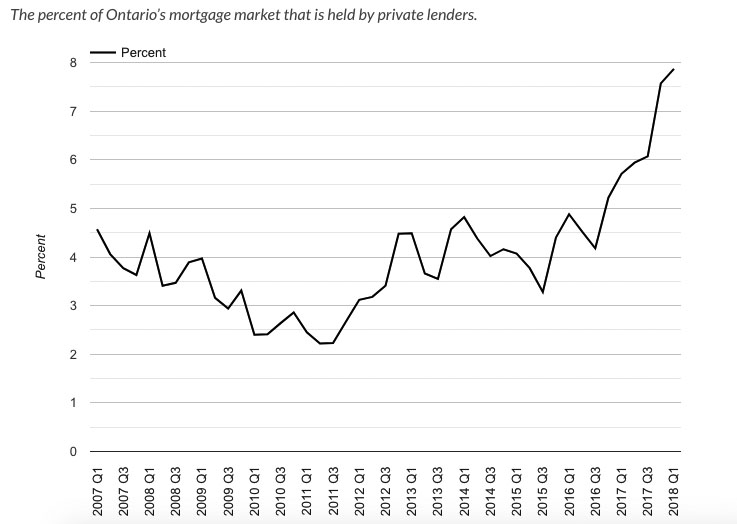

By mid 2018 over 7.87% of the Canadian mortgage market was held by private lenders – a 37.8% increase compared to the same quarter the previous year. That number has most certainly since surpassed 8%. With private lending becoming such a significant part of the mortgage landscape, it’s important that more people understand the benefits and drawbacks of them before being advised to use them.

Benefits of Using a Private Lender

The most obvious benefit to using a private lender is convenience. With much less stringent requirements, both from government regulations and their own internal requirements, private lenders are free to lend money to just about anyone they want to. They’ve become the option of choice for mortgage brokers and agents who have clients with damaged credit trying to consolidate debts. While a private lender does charge much higher rates than banks, they’re usually far lower than credit card rates.

Investors have also been flocking to private lenders for years to fund their projects. Banks traditionally don’t want to fund flip projects or student rentals because of the uncertainty and higher perceived risk; but they can be quite lucrative for private lenders. As long as the investor has a clear exist strategy and can prove they can cover the higher rates and have an exit strategy for repaying the full mortgage, a private lender will often overlook an investor’s income, debt servicing, credit scores or portfolio size.

Private loans also bridge a gap in types of properties that traditional lenders don’t want to deal with – cottages without running water, farms, vacant or raw land, construction or renovation projects. These are all traditionally difficult to do with a bank if they don’t have an existing program for it, but a private lender will use more common sense to evaluating the project and listen to the reasons for the loan.

Because the costs to use a private lender are much higher, they’re typically used for short term solutions. In the case of the investor they’re often only used for a couple months before being paid back with a sale or refinance when the project is complete. Debt consolidating borrowers will often use a private lender to access a second mortgage to consolidate debts when breaking their existing mortgage carries too many fees and penalties. In this case the private second mortgage will often be paid out when it’s time to refinance the existing first mortgage.

This leads to another benefit of private mortgages is that they’re typically open mortgages and can be paid out at any time after the first 30 or 60 days.

Drawbacks of Using a Private Lender

The biggest drawback is typically the cost. With borrowers flocking to privates because of increasing interest rates and challenges qualifying under the stress test, private lenders have benefited from the increased demand and have responded by increasing their rates.

Currently borrowers looking for a private 1st mortgage can expect to pay between 7-10% interest with an additional 1-4% broker/lender fee. 2nd mortgages are currently typically 9-14% with a 2-5% broker/lender fee. Since private lenders do not pay a finder’s fee to the mortgage broker arranging the mortgage like a bank will, brokers and agents need to charge their fee on top of the private lender rate and fee, otherwise find themselves spending hours arranging the mortgage for free.

Another drawback to working with private lenders is they typically only offer 1-year terms. That means when the year is up the borrower will need to refinance the mortgage elsewhere or sign a renewal and pay a fee again. This is a challenge when a borrower may be looking to consolidate debts and has a year and a half on their current mortgage. The borrower will need to either extend the private an additional six months, or break their current mortgage six months early. An investor may have an issue if they’re unable to refinance the property with a traditional lender or are unable to sell quickly enough. They’ll need to hold the mortgage longer than they budgeted for.

Sill another drawback to working with a private lender is that they typically set their own rules and will charge as much as they feel the market will allow to maximize profits. It also means that they have more freedom to cancel or turn down an application at any stage. Many mortgage agents will have at least a few horror stories about private lenders increasing their fee or cancelling the loan at the last minute, leaving the borrower and mortgage broker scrambling.

This is less common with large MICs and institutional private lenders as they rely on they reputation with brokers to bring them clients, but it does happen for a range of reasons. It is also known to happen with banks and the reasoning is often issues with the condition of the property or other unforeseen issues.

Work With a Reputable Mortgage Broker or Agent

With private lenders having a much larger pool of borrowers to choose from with far less restrictions than traditional lenders, it’s important to ensure borrowers working with a reputable mortgage agent and broker. It’s important to understand that when presented with a mortgage commitment from a broker, borrowers are signing a legal document.

While all fees need to be disclosed up front, it’s relatively easy for lenders and brokers to include fees and not clearly point them out. There’s also fees, clauses and terms that are decided on by the lender that protect their interests and unscrupulous lenders can use them to aggressively charge fees and penalties that borrowers are bound to pay.

A reputable mortgage broker will have a set list of reputable private lenders they use regularly and will understand their terms to ensure they’re fair. A less reputable or inexperienced broker may find themselves scanning online classifieds looking for a private lender and won’t know in advance what the mortgage terms will be. A real estate lawyer will be able to review a mortgage commitment for anything that may be excessing or overly punitive.

For more information on working with myself or private lenders, feel free to reach out – Steve@SteveWhiteMortgages.ca or 905.903.4799